Digital payments have made business transactions faster and more convenient than ever. But with this speed comes a growing risk of fraud that looks completely legitimate.

What if a scammer could trick you into sending money yourself willingly, without any alarms going off?

That’s exactly what Authorized Push Payment (APP) fraud is. APP fraud is one of the fastest-growing threats in this space. Unlike traditional fraud, these attacks don’t rely on system vulnerabilities; they rely on trust, urgency, and human error.

And the numbers are alarming. According to Deloitte, APP fraud losses in the US alone could hit nearly $15 billion by 2028.

In this blog, we will discuss everything about APP fraud and what businesses can do to ensure that they stay protected against.

What is Authorized Push Payment fraud?

Authorized Push Payment (APP) fraud happens when a person or business is tricked into sending money to a fraudster, believing the payment is legitimate.

The key point is that the payment is approved by the payer, but based on false information. The APP fraud is tricky to manage because the owners themselves approve the payment, and there are no hints of fraud in the entire money transfer process

Let us take an example to understand:

Authorised Push Payment (APP) fraud begins with a deception so convincing that no alarm bells ring: a spoofed email from a known supplier, the right logo, the right tone, the right level of urgency, asking your finance team to update bank details before an upcoming payment.

Everything checks out, the approval goes through, and the transfer lands exactly where it was intended: in the hands of a fraudster.

Hours later, the real supplier calls to follow up on the invoice, and the ground shifts. They never sent that email. The account was never theirs. The money is already gone, and because every step of the transaction was willingly authorised by a real person acting in genuine good faith, it falls into one of the most difficult categories of financial crime to recover from — not a hack, not a system breach, but a manipulation of trust so precise that the victim became the instrument of the theft.

Push payment vs pull payment – Comparison

Every business payment falls into one of two types. The type decides who controls the money, who takes the risk, and how easy it is to get the money back if something goes wrong.

This is not a small detail. It helps explain why authorised push payment fraud is very hard to reverse. It also shows why bank fraud controls, which are mostly built for a different type of payment (pull payments), do not protect businesses as much as many owners think.

| Aspect | Push Payment (APP Context) | Pull Payment |

| Who initiates the payment | You (payer) send the money | Merchant/service collects the money |

| Control | Fully controlled by the payer | Controlled by the merchant (with consent) |

| How it works | Money is transferred directly to another account | Money is deducted from your account |

| Examples | Bank transfer, UPI payment | Card payments, subscriptions |

| Fraud risk | Higher in APP fraud (payer is manipulated) | Lower due to built-in protections |

| Reversibility | Hard to reverse once sent | Easier (chargebacks/refunds possible |

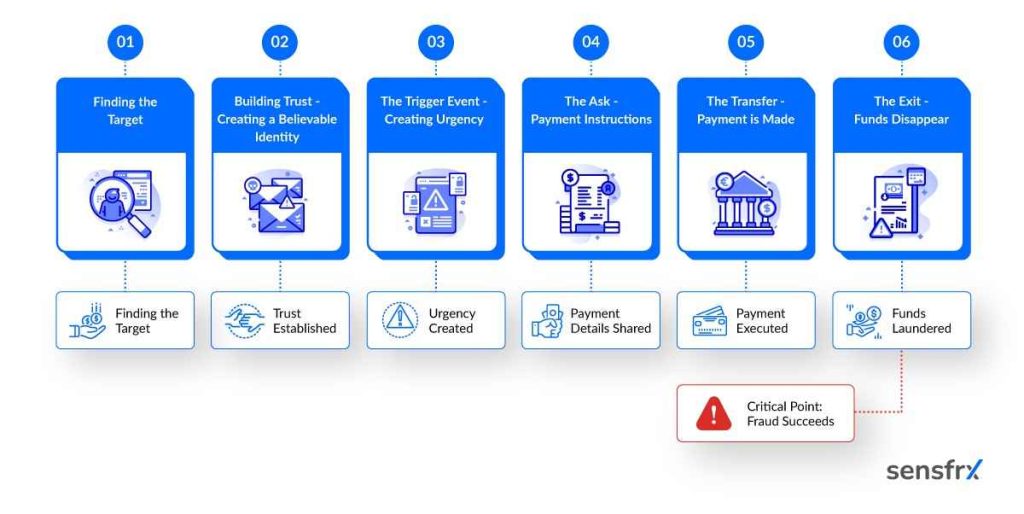

Most Authorized Push Payment (APP) fraud attacks follow a predictable pattern. Understanding these stages helps businesses identify where intervention is possible.

The Anatomy of Push Payment Fraud

Step 1: Finding the Target: Fraudsters start by gathering information about the victim. This can come from:

- Social media profiles

- Data breaches

- Professional platforms

Example: A fraudster identifies a company’s finance manager on LinkedIn and learns about their role and vendors.

Step 2: Building Trust — Creating a Believable Identity

The attacker impersonates a trusted entity using:

- Spoofed email domains

- Fake websites

- Lookalike phone numbers

Example: An email appears to come from a known supplier, using a nearly identical domain name.

Step 3: The Trigger Event — Creating Urgency

A situation is created to push quick action:

- “Urgent invoice update”

- “Security issue with your account”

- “Limited-time investment opportunity”

Example: The finance team is told that payment must be made immediately to avoid service disruption.

Step 4: The Ask — Payment Instructions

Clear and convincing payment details are shared:

- New bank account information

- Revised beneficiary details

Example: “Please send all future payments to this updated account due to internal changes.”

Step 5: The Transfer — Payment is Made

The victim initiates the payment, believing it is legitimate. Since it’s a push payment, the transaction is authorized. This is the critical point where fraud succeeds.

Step 6: The Exit — Funds Disappear

The money is quickly moved through multiple accounts (often mule accounts), making recovery difficult.

Example: Funds are split and transferred across different accounts within minutes.

Types of APP Fraud

APP fraud isn’t a single threat; it’s a growing family of scams, each exploiting a different vulnerability. Some have been around for a long time and feel familiar. But with the advent of AI APP fraud is evolving faster than most fraud defenses can keep up with.

The Well-known Types

Purchase scams are the most common ones. More than half of consumers surveyed reported experiencing a shopping scam in 2024, including fraudulent listings, fake sellers, and goods that never arrived.

Investment scams have become a serious financial threat. UK consumers alone lost an estimated £98 million to investment fraud in just the first half of 2025.

Romance scams involve building fake relationships before eventually requesting money transfers. In the United States alone, the Federal Trade Commission reported that romance scams led to losses of over $1.4 billion in 2023. Additionally, these scams tend to be among the most expensive for victims, with a median loss exceeding $2,000 per person.

Impersonation scams involve criminals posing as trusted authorities such as banks, HMRC, or the IRS, or law enforcement to pressure victims into urgent payments.

Invoice and mandate fraud typically targets businesses, where payment details on legitimate invoices are quietly swapped out, redirecting funds to a fraudster’s account.

The Emerging Threats

These are the scam types growing fastest and the ones most fraud strategies are least prepared for.

A. AI Deepfake-Enabled APP Fraud

Generative AI has made it much easier for fraudsters to trick people. They can now copy someone’s voice to pretend to be a company executive on calls or use fake videos on apps like Microsoft Teams and Zoom to look real during meetings. What used to need advanced technical skills can now be done easily and on a large scale.

B. Business Email Compromise (BEC)

BEC is a combination of social engineering and financial fraud. US businesses lost $2.7 billion to BEC in 2024 alone, not through system breaches, but through employees being manipulated into bypassing standard procedures and authorizing transfers to fraudulent accounts.

C. Pig Butchering

Pig butchering is long-con investment fraud built on emotional manipulation. Scammers spend weeks or months building trust through dating apps or social media, carefully grooming victims before introducing a “exclusive” investment opportunity. By the time the victim realizes the platform is fake, the money is gone.

D. Crypto-Specific APP Fraud

Cryptocurrency has become a preferred destination for proceeds of APP fraud and there is a growing need for cryptocurrency fraud prevention. Nearly $10 billion in crypto was lost to scams in 2024. The appeal for fraudsters is straightforward: transactions are largely irreversible, and the perceived anonymity makes recovery and prosecution significantly harder.

Who is at risk?

Small and Medium-Sized Businesses (SMEs)

SMEs are a prime target because they move money regularly but rarely have the fraud controls that larger companies do. A fake invoice that looks like it came from a trusted supplier. A sudden request to update payment details. An email that appears to be from a senior manager asking for an urgent transfer. These are everyday scenarios that catch small business teams off guard.

The core problem is that the employees who have the authority to make payments often have no verification process to follow before doing so. One approved transfer to the wrong account can cost a business thousands, sometimes more.

Corporate and Enterprise Businesses

For large organizations, fraud isn’t random; it’s targeted, researched, and highly convincing. Attackers study leadership structures, vendor relationships, and internal workflows before striking.

BEC (Business email compromise) and supply chain fraud work not just because the emails look real, but because they exploit organizational psychology, specifically the pressure not to slow down a senior leader or delay a critical vendor payment. The attacker doesn’t need to break your security stack; they need to break your approval culture.

What makes large organizations particularly vulnerable

- Complexity hides anomalies. In a company processing thousands of transactions, a single fraudulent wire can hide in the noise until the month-end reconciliation.

- Siloed verification. Finance may not know the CEO’s travel schedule, so an “I’m in a meeting, handle this quietly” email isn’t easily cross-checked.

- Vendor relationship age. Long-standing suppliers are trusted implicitly — attackers specifically target these because “we’ve worked with them for years” short-circuits

Crypto Investors

Crypto users face a unique and particularly frustrating challenge. Most platforms used by scammers are unregulated, which means there is little to no consumer protection in place. Once funds are transferred into a crypto wallet, tracing or recovering them is nearly impossible. There is no bank to call, no chargeback to file, and no regulator to escalate to.

Individual Consumers

Every day, people are often the easiest targets, particularly older adults. They typically have higher savings, are less familiar with digital payment systems, and are more likely to trust an unexpected call or message. Scammers exploit this by using spoofed caller IDs, creating a false sense of urgency, and triggering fear, such as warning someone that their bank account has been compromised. By the time the victim realizes something is wrong, the money is already gone.

The Bottom Line for Business Owners

If you run a business of any size, then you are a target. The common thread across every category above is trust. APP fraud works because it exploits the trust we place in familiar names, known contacts, and routine processes. Understanding who is vulnerable is the first step toward making sure your business is not next.

The Psychology Behind APP Fraud

APP fraud does not just trick systems; it tricks people. And it does so by targeting very human instincts.

- Authority bias makes us comply when someone sounds official. A caller claiming to be from your bank, the police, or a government agency instantly lowers our guard.

- Urgency and scarcity shut down rational thinking. When someone tells you to act now or face consequences, there is no time to pause and verify.

- Social proof removes doubt. Phrases like “your colleague already approved this” make an unusual request feel normal and pre-validated.

- Fear and loss aversion push people to act out of panic rather than logic. The threat of a frozen account or legal trouble is enough to make even careful people move fast.

- Love bombing, used in romance scams, builds deep emotional trust over weeks or months and then makes the eventual request for money feel completely natural.

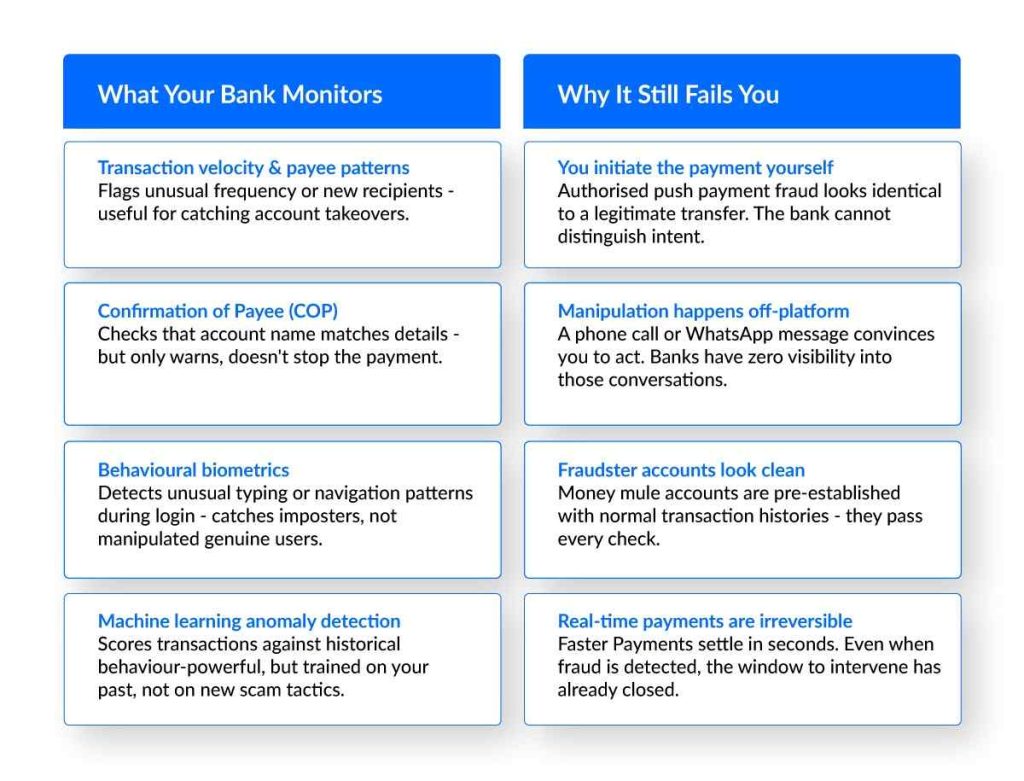

How Banks Detect (and Miss) APP Fraud

Banks or financial bodies have fraud prevention techniques in place, but still, APP fraud is still missed in a lot of cases. Below is a quick comparison that explains what bank monitors are and why it still fails you.

What To Do Immediately If You’ve Been Defrauded?

Time-sensitive steps:

- Within minutes: Contact your bank’s fraud line — request a recall/freeze

- Within 1 hour: Report to national fraud authority (Action Fraud UK / FTC US / ACCC Australia)

- Within 24 hours: File a formal complaint citing the reimbursement scheme applicable in your jurisdiction

- Document everything: Screenshots, emails, call logs, transaction references

- Report to police — needed for formal investigation and insurance claims

- Notify your employer if a business account was involved

- Check for identity compromise — change passwords, enable MFA

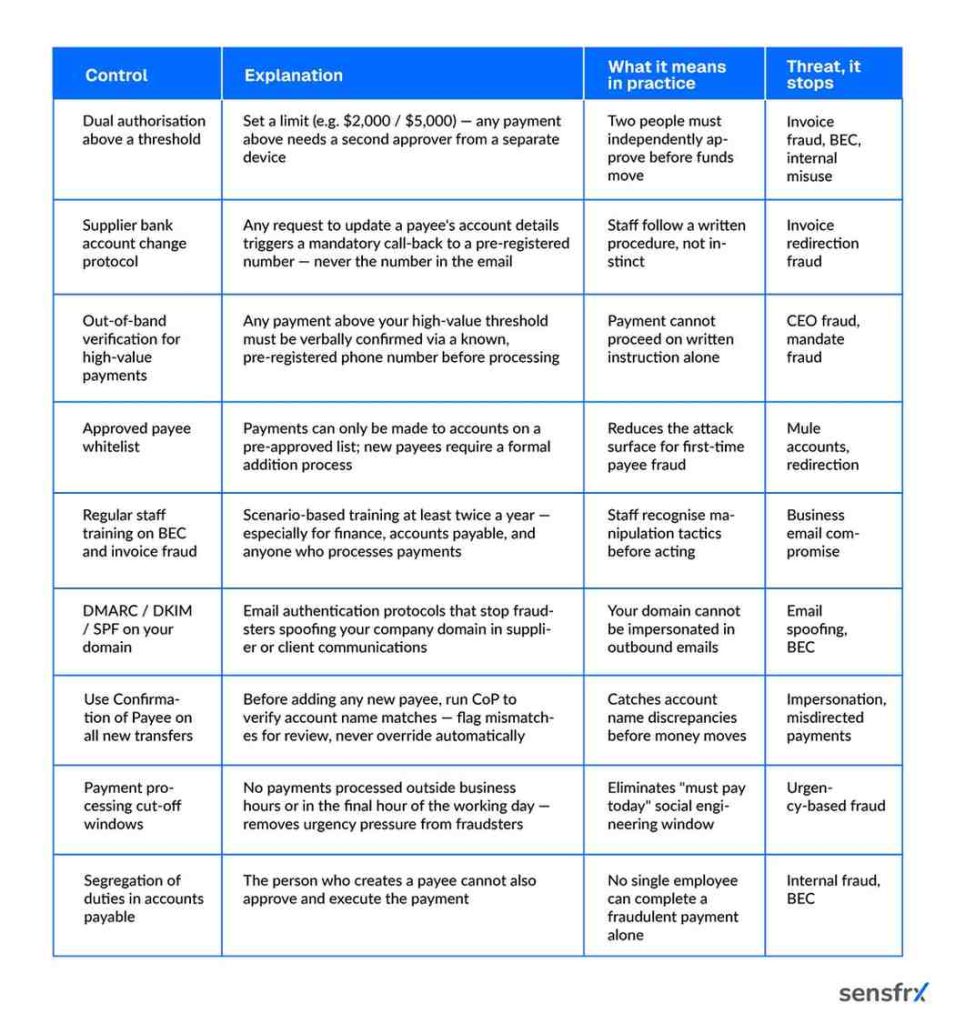

Prevention Checklist for Businesses

If businesses become a victim of a push payment fraud, then the losses can be humongous. So, having preventive measures in place can help ward off these threats to some extent.

Below is a detailed checklist of the controls that you can put in place to prevent any type of issues:

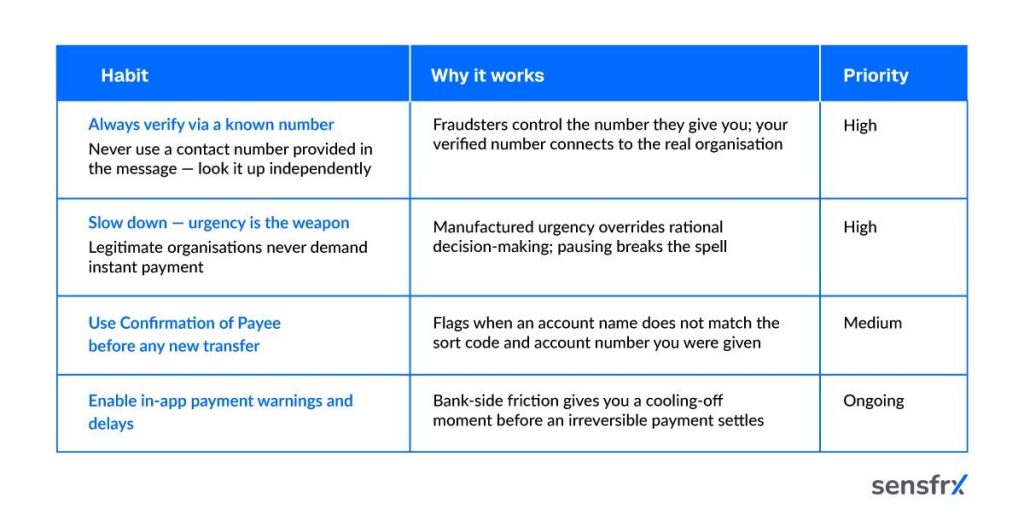

Checklist for Individuals

Individuals can also be victims of push payment fraud, so they need to be aware of what they can do to prevent it from happening.

Future of APP Fraud

1. AI makes social engineering scalable and convincing

Deepfake audio and video now allow fraudsters to impersonate a CEO or finance director in real time. Personalised phishing scripts built from LinkedIn and Companies House data cost almost nothing to produce at scale. Businesses relying on voice familiarity or email tone as trust signals will find those cues increasingly unreliable.

Deloitte’s aggressive-scenario forecast for US APP fraud losses rising from $8.3B in 2024 to $18.2B by 2028 if AI-driven attacks outpace defences

2. Real-time payment adoption will widen the fraud window globally

As instant payment rails expand across the US (FedNow), EU (SEPA Instant), and Asia, the no-intervention window that makes APP fraud so effective will spread to new markets. Businesses operating internationally will face the same irreversibility risk across every currency they transact in.

3. Cross-industry coalitions are setting the US standard

The Aspen Institute’s National Task Force for Fraud and Scam Prevention unites 33 cross-industry players that include banks, telecoms, tech firms, and federal agencies to develop a coordinated US response. The bipartisan TRAPS Act (proposed June 2025) separately aims to establish a federal task force on digital payment scams. $14.9B is the Deloitte baseline forecast for US APP fraud losses by 2028.

Conclusion

Authorized Push payment fraud is not just a technology problem — it is a manipulation problem. Fraudsters rarely hack into bank systems directly; instead, they trick people into willingly sending money to fraudulent accounts.

The threat continues to grow as AI-powered scams become more convincing, instant payment systems leave little time to react, and sophisticated fraud tools become easily accessible online.

The pattern is always the same: someone is rushed into sending money to a new account without double-checking. Businesses that stop this are the ones that make it structurally hard to do, not the ones hoping their bank catches it.

That’s where SensfrX helps. By identifying signs of pressure, urgency, and suspicious behavior in real time, SensfrX helps stop fraudulent transactions before payments are processed. Sign up for a free SensfrX trial today and strengthen your defense against push payment fraud.

What is Authorized Push Payment (APP) fraud?

Authorized Push Payment fraud happens when a scammer tricks a person or business into willingly sending money to a fraudulent account. Unlike account hacking, the victim authorizes the payment themselves after being manipulated through impersonation, fake invoices, investment scams, or urgent requests.

What are the most common types of APP fraud scams?

The most common APP fraud scams include:

• Business email compromise (BEC)

• Fake invoice or supplier payment scams

• Bank impersonation scams

• Investment and cryptocurrency scams

• Romance scams

• Tech support scams

• CEO fraud targeting employees

Fraudsters usually create urgency and pressure victims into acting quickly before verifying payment details.

How can businesses prevent Authorized Push Payment fraud?

Businesses can reduce APP fraud risk by:

• Verifying bank account changes through secondary channels

• Using multi-person payment approvals

• Monitoring behavioral and transaction anomalies

• Training employees to detect phishing and impersonation attempts

• Implementing fraud detection tools with device intelligence and risk scoring

• Flagging unusual payment requests in real time

Layered fraud prevention is important because APP fraud relies heavily on social engineering rather than stolen credentials alone.

Can victims recover money lost to APP fraud?

Recovery depends on the payment method, bank policies, local regulations, and how quickly the fraud is reported. In many cases, victims have limited protection because they technically authorized the payment themselves. Some regions now require reimbursement under specific conditions, especially for consumer accounts. Immediate reporting greatly improves the chances of freezing funds before withdrawal.

Why is Authorized Push Payment fraud increasing so rapidly?

APP fraud is growing because:

• Real-time payments are instant and difficult to reverse

• Fraudsters use advanced social engineering tactics

• Digital banking and online payments are increasing

• AI-generated impersonation and phishing techniques are becoming more convincing

• Consumers and employees often trust urgent requests from seemingly legitimate sources